Download Here: https://www.constantcommercial.com/news-and-insights

The purpose of this article is to describe and illustrate Constant Commercial’s complimentary Real Estate Valuation (REV) tool and the basic underwriting required. The download is available on Constant Commercial Real Estate’s website in the NEWS & INSIGHTS tab. The REV can be used for commercial, multifamily, single family portfolios and short-term rental properties where the income approach is applicable. Valuation methods are briefly discussed before using a sample 10-unit multifamily building as an illustration.

There are three real estate valuation methods. The three methods are the comparable sales approach, cost approach and income approach. When valuing real estate it is important to understand the differences and how an investor and appraiser/underwriter may use one, two or all three valuation methods to determine market value.

The comparable sales approach uses recent sales of similar property size and type. An underwriter would value aspects seen in comparable sales to refine a price per square footage figure to use for the subject property being valued. For example, an adjustment would be made to a recent sale that has an extra half bathroom, bedroom, garage, larger lot or any other aspect that helps contribute or take away value to the subject property. Ultimately, the underwriter is refining a price per square foot.

The cost approach describes a valuation method that accounts for the value of the land and cost to build the same structure. This is a reliable valuation method for unique properties and areas with few comparable sales. The cost approach will take into consideration the principle of substitution, replacement cost, reproduction cost, direct/indirect costs, entrepreneurial profit, depreciation and curable/incurable physical deterioration.

The third valuation method is the income approach. A Capitalization rate is used to value the income properties Net Operating Income (NOI). To determine capitalization rates the investor and underwriter requires an understanding of the market, property type, size and condition. The capitalization rate (a no debt return metric) converts the NOI into an estimation of value. The subject properties capitalization rate can vary so consult with a professional when using capitalization rates for your market and ensure underwriting is performed with realistic inputs and capitalization rates are from quality data. Income approach is most often used for Commercial and Multifamily (5+ Units) property types. For 2-4 unit properties (considered residential), the comparable sales approach may convolute the valuation.

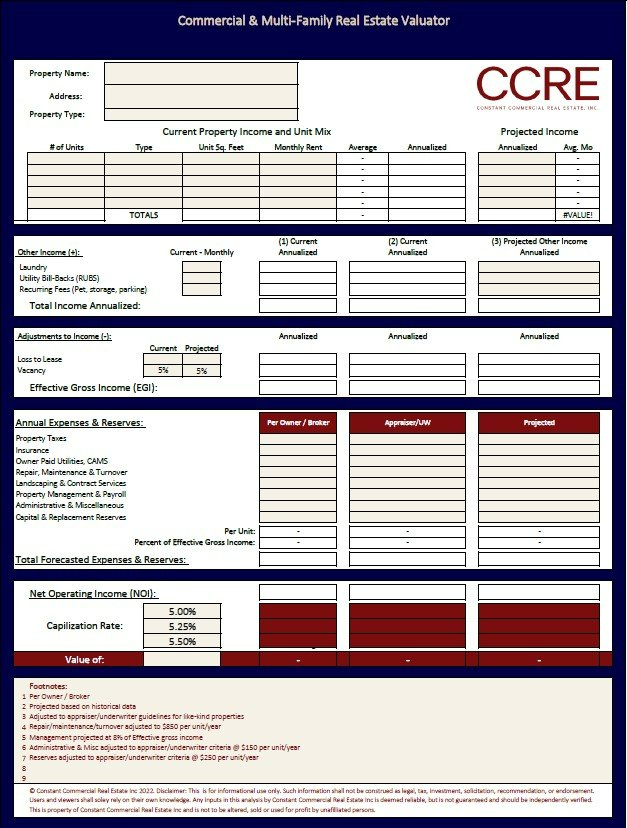

The Real Estate Valuator (REV) can be broken down into seven parts. When all tan input cells are filled out, the REV will calculate up to 12 values to gather a pulse on the variables affecting current and projected valuations. The seven parts are:

1. Property name, address and type

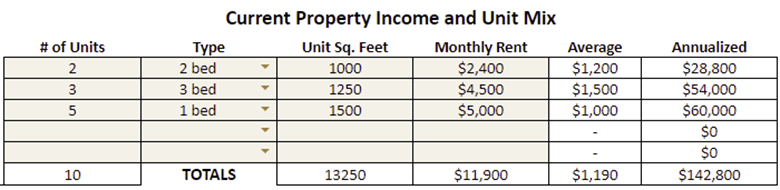

2. Unit Mix and Current & Projected Property Income

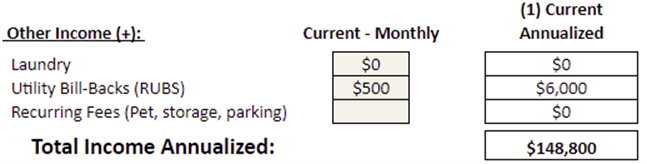

3. Other Income (+)

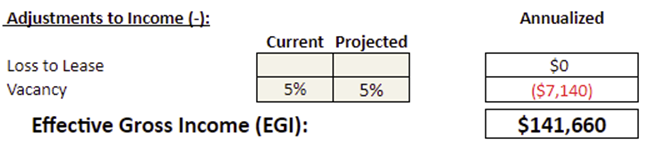

4. Adjustments to Income - Loss to Lease & Vacancy (-)

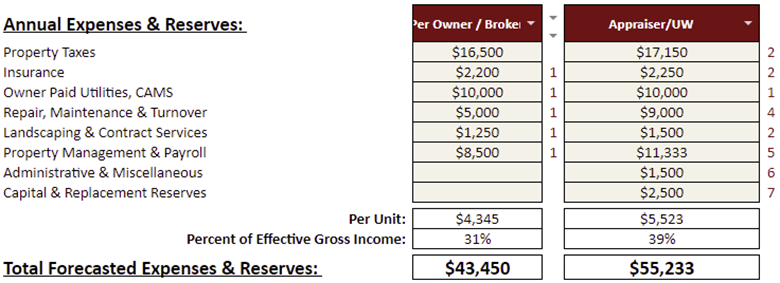

5. Annual Expenses

6. Capitalization Rate & Value

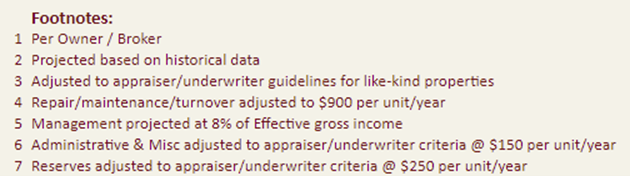

7. Footnotes

Notice the three column layout of the tool. This allows the underwriter to justify two scenarios on current rents with different expense loads. With buyer clients our advisors will oftentimes use the first (left) column with the seller or listing brokers (“Per Owner/Broker”) offering memorandum and provided income and expenses to express an understanding of their asking price. The middle column can then be adjusted to use an adjusted expense load that is more realistic or an appraiser/underwriter would use. The furthest right column can be used for a variety of other scenarios but often is reflecting a projected/pro-forma scenario following building stabilization. The same tool can be used with sellers to justify how value changes with lower expense loads and raising income for developing a sale strategy and exit.

10-unit Multifamily Illustration -

Step 1: Calculate the Effective Gross Income –

Effective gross income is the total income an investor can expect to receive from the property. An investor can use past or current scheduled income to start. Then add “other income”. Only recurring income beyond the stated monthly rent is accepted by the lender/appraiser. These fees are oftentimes utility bill-backs (RUBS), laundry, pet rent and parking. Late fees, or deposits forfeited are NOT other income as they are non-recurring. Next deduct vacancy loss from turnover and vacancies. Generally, appraisers/underwriters will use 5%. Some lenders have their own criteria whether they will use 5%, 10% or the economic vacancy (actual present vacancy rate).

Effective Gross Income (EGI) = Total Rents + Other Income - Vacancy (X%)

Annualized rents = $142,800 ($1,190 per unit)